(Editor’s note: This post is part of a series covering YTF’s work with the United Nation’s Sustainable Development Goals. See more of the series here.)

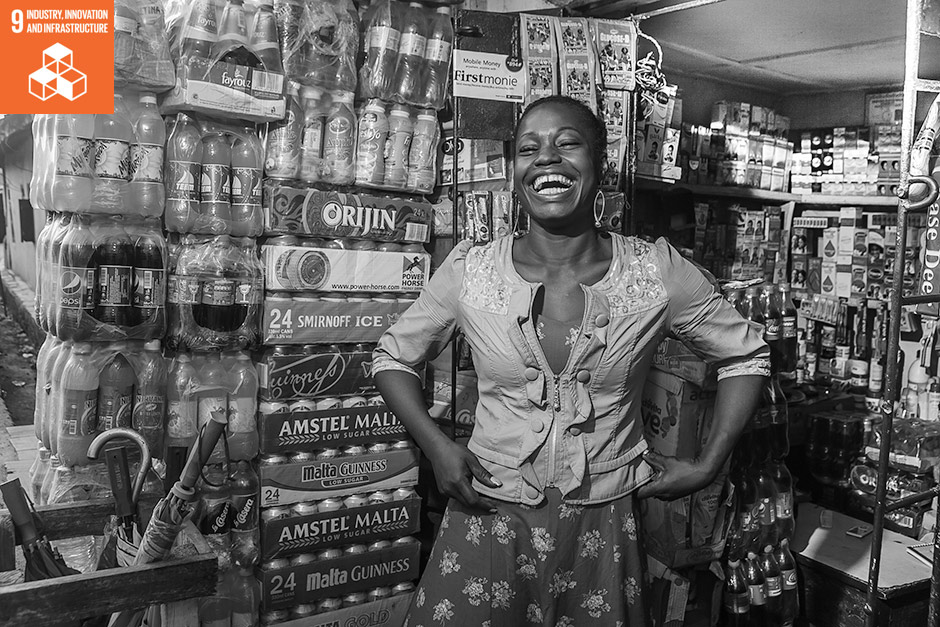

Entrepreneurship is the catalyst for Africa’s sustainable economic growth—however, women entrepreneurs are often barred from full participation in the economy due to disparities in financial inclusion and infrastructure issues. Barriers include: 1) access to financing, formal bank accounts and financial services, credit, and capital, 2) gender bias-based government regulations that hinder business expansion, growth, and transactions, 3) limited school-based business and financial skills training, 4) lack of proof of identity, and 5) the lack of business networks and female entrepreneur mentors to support and strengthen women-owned micro-, small-, and medium-sized enterprises (MSMEs).

Example: Nigeria. Although women entrepreneurs account for nearly half of the ownership of micro-enterprises, female ownership of small- or medium-sized enterprises drops with only 23% female ownership—a 90% disparity between female-owned and male-owned SMEs.[1]

Nigeria’s women entrepreneurs are underserved and isolated from participation in the financial sector, and need training, mentoring, and resources to build business development abilities, financial management capacities, and financial sector inclusion rates. YTF’s experience and research demonstrates that women-owned businesses are excluded by micro-finance organizations and commercial banks, despite proven capacities as sustainable revenue generators.

Top barriers to business development in Nigeria are access to finance (30% of World Bank 2015 Enterprises Survey respondents) and electricity (27%). Access to finances is identified by 57% of firms with female top management as a major constraint—much more than firms with male top management (32%). Rejection of loan applications in Nigeria occurs 250% more often in firms whose top management is female than male—this compares to a 15% loan rejection rate for both female and male top management in Sub-Saharan Africa.

Business losses due to outages are two-three times more in Nigeria than Sub-Saharan Africa.[2] Teaching women entrepreneurs to utilize mobile phones for business purposes can more than compensate for these losses. Nigeria has greatly increased in the availability of mobile phone subscriptions, from 27.5/100 persons in 2006 to 77.8% in 2013. More recent research (2014) shows that cell phones are as common in Nigeria as they are in the U.S. with 89% of the population of each country having a cell phone.[3]

Mobile Financial Services for Women. YTF partners with public and private entities to train women entrepreneurs in financial and business skills development which has resulted in women increasing access to financial services, attaining business loans and financing, opening checking and savings accounts, using electronic payments, and networking with other women entrepreneurs—this has allowed them to increase business strategies, add products or services, hire more employees, increase annual revenue, grow from micro- to small- or medium-sized enterprises and integrate the use of mobile business and financial strategies.